If you’ve been involved in forex trading for any time the chances are you’ve heard ofMartingale. But what is it and how does it work? In this post, I’m going to talk about the strategy, it’s strengths, risks and how it’s best used in the real world.

There’s a few reasons why this strategy is attractive to currency traders.

Firstly it can, under certain conditions give a predictable outcome in terms of profits. It’s not a sure bet, but it’s about as close as you can get.

Secondly it doesn’t rely on an ability to predict absolute market direction. This is useful given the dynamic and volatile nature of foreign exchange. It yields a better return the more skillful you are. But it can still work when your trade picking skills are no better than chance.

And thirdly, currencies tend to trade in ranges over long periods – so the same levels are revisited over many times. As with grid trading, that behavior suits this strategy.

The important thing to know about Martingale is that it doesn’t increase your odds of winning. Your long-term expected return is still the same. It’s governed by your success in picking winning trades. You can’t escape from that.

What the strategy does do is delay losses. Under the right conditions, losses can be delayed by so much that it seems a sure thing.

How It Works

In a nutshell: Martingale is a cost-averaging strategy. It does this by “doubling exposure” on losing trades. This results in lowering of your average entry price. The idea is that you just go on doubling your trade size until eventually fate throws you up one single winning trade. At that point, due to the doubling effect, you can exit with a profit.

A Simple Win-Lose Game

This simple example shows this basic idea. Imagine a trading game with a 50:50 chance of winning verses losing.

| Stake | Outcome | Profit/Loss | Running Balance |

| $1 | Win | $1 | $1 |

| $1 | Win | $1 | $2 |

| $1 | Lose | -$1 | $1 |

| $2 | Lose | -$2 | -$1 |

| $4 | Lose | -$4 | -$5 |

| $8 | Win | $8 | $3 |

Copyright © 2015 Forexop.com

Table 1: Simple betting example.

I place a trade with a $1 stake. On each win, I keep the stake the same at $1. If I lose, I doublemy stake amount each time. Gamblers call this doubling-down.

If the odds are fair, eventually the outcome will be in my favor. And since I’ve been doubling my stake each time, when this happens the win recovers all of the previous losses plus the original stake.

This is thanks to the double-down effect. Winning bets always result in a profit. This holds true because of the fact that 2n = ∑ 2n-1 +1. That means the string of consecutive losses are recovered by the winning trade.

If you’re interested in experimenting with the toy system, here is my simple betting game spreadsheet:

A Basic Trading System

In real trading there isn’t a strict binary outcome. A trade can close with a certain profit or loss. But this doesn’t change the basic the strategy. You just define a fixed movement of the underlying rate as your take profit, and stop loss levels.

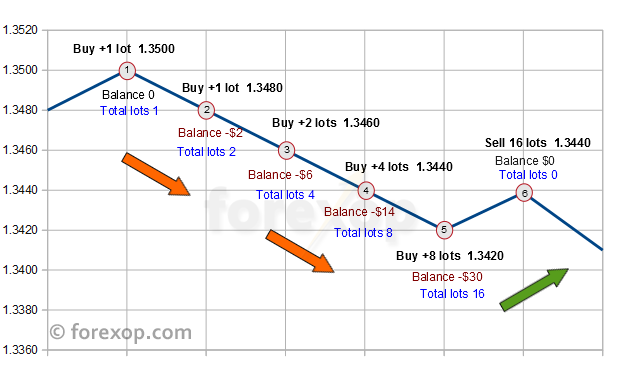

The following case shows this in action. I’ve set my take profit and stop loss at 20 pips.

| Rate | Order | Lots (micro) | Entry | Avg. Entry | Abs. Drop (pips) | Break Even (pips) | Balance $ |

| 1.3500 | Buy | 1 | 1.3500 | 1.3500 | 0.0 | 0.00 | $0 |

| 1.3480 | Buy | 2 | 1.3480 | 1.3490 | -20.0 | 10.00 | -$2 |

| 1.3460 | Buy | 4 | 1.3460 | 1.3475 | -40.0 | 15.00 | -$6 |

| 1.3440 | Buy | 8 | 1.3440 | 1.3458 | -60.0 | 17.50 | -$14 |

| 1.3420 | Buy | 16 | 1.3420 | 1.3439 | -80.0 | 18.75 | -$30 |

| 1.3439 | Sell | 16 | 1.3439 | 1.3439 | -61.2 | 0.00 | $0 |

Copyright © 2015 Forexop.com

Table 2: Averaging down trade entry levels in falling market.

I start with a buy to open order of 1 lot at 1.3500. The rate then moves against me to 1.3480 giving a loss of 20 pips. It reaches my virtual stop loss.

It’s a virtual stop loss because there would be no point in closing the trade, and opening a new one for twice the size. I keep my existing one open on each leg and add a new trade to double the size.

So at 1.3480 I double my trade size by adding 1 more lot. This gives me an average entry rate of 1.3490. My loss is the same, but now I only need a retracement of +10 pips to break even rather than 20 pips as before.

The act of “averaging down” means you double your trade size. But you also reduce the relative amount required to re-coup the losses. This is shown by the “break even” column in Table 2.

The break-even approaches a constant value as you average down with more trades. This constant value gets ever closer to your stop loss. This means you can catch a “falling market” very quickly and re-coup losses – even when there’s only a small retracement (see Figure 1).

At trade #5, my average entry rate is now 1.3439. When the rate then moves upwards to 1.3439, it reaches my break-even.

I can close the system of trades once the rate is at or above that break even level. My first four trades close at a loss. But this is covered exactly by the profit on the last trade in the sequence.

The final P&L of the closed trades looks like this:

| Order | Lots | Entry | P&L |

| Buy 1 | 1 | 1.3500 | -$6.12 |

| Buy 2 | 1 | 1.3480 | -$4.12 |

| Buy 3 | 2 | 1.3460 | -$4.25 |

| Buy 4 | 4 | 1.3440 | -0.50 |

| Buy 5 | 8 | 1.3420 | $15.00 |

| Totals | 16 | $0.00 |

Copyright © 2015 Forexop.com

Table 3: Losses from previous trades are offset by the final winning trade.

Does Martingale Always Work?

In a pure Martingale system no complete sequence of trades ever loses. If the price moves against you, you simply double the size of the trade.

But such a system can’t exist in the real world because it means having an unlimited money supply and an unlimited amount of time. Neither of which are achievable.

In a real trading system, you need to set a limit for the drawdown of the entire system. Once you pass your drawdown limit, the trade sequence is closed at a loss. The cycle then starts again.

When you restrict the ability to drawdown, you’re departing from a true Martingale system. And in doing so you’re using an approximation that’s prone to catastrophic failure.

Doubling-down verses Probability of Loss

Ironically, the greater your drawdown limit, the lower your probability of making a loss – but the bigger that loss will be. This is the Taleb dilemma.

The more trades you do, the more likely it is that those extreme odds will “come up” – and a long string of losses will wipe you out.

In Martingale the trade exposure on a losing sequence increases exponentially. That means in a sequence of N losing trades, your risk exposure increases as 2N-1. So if you’re forced to exit prematurely, the losses can be truly catastrophic.

On the other hand, the profit from winning trades only increases linearly. It’s proportional to half the profit per trade multiplied by total number of trades.

Winning trades always create a profit in this strategy. So if you pick winners 50% of the time (no better than chance) your total expected return from the winning trades would be:

E ≈ ½ N x B

Where N is the number of “trades” and B is the amount profited on each trade.

But your big one off losing trades will set this back to zero. For example, if your limit is 10 double-down legs, your biggest trade is 1024. You would only lose this amount if you had 11 losing trades in a row. The probability of that is (1/2)11. That means, every 2048 trades, you’d expect to lose once.

So after 2048 trades:

- Your expected winnings are (1/2) x 211 x 1=1024

- Your expected one off loss is -1024

- Your net profit is 0

So your odds always remain 50:50 within a practical system. That’s assuming your trade picking is no better than chance.

Your risk-reward is also balanced at 1:1. But in this strategy your losses will all come in one big hit. So it may seem far worse than it is, especially if you’re unlucky!

Martingale can’t improve your odds of winning. It just postpones your losses. See Table 4.

| #Trades | Expected winnings | Expected loss (1 off event) | Net (average) |

| 1 | 0.5 | -0.5 | 0 |

| 2 | 1 | -1 | 0 |

| 4 | 2 | -2 | 0 |

| … | … | … | … |

| 512 | 256 | -256 | 0 |

| … | … | … | … |

Copyright © 2015 Forexop.com

Table 4: Your winning odds aren’t improved by Martingale. Your net return is still zero.

Those people who’re trend followers at heart often believe it’s better to use a reversal the Martingale. The anti-Martingale or reverse Martingale tries to do the exact opposite of what’s described above. Basically these are trend following strategies that double up on wins, and cut losses quickly.

Stay Away from “Trending” Currencies

The best opportunities for the strategy in my experience comes about from range trading. And by keeping your trade sizes very small in proportion to your capital, that is using very low leverage. That way, you have more scope to withstand the higher trade multiples that occur in drawdown.

There are dozens of other views however. Some people suggest using Martingale combined with positive carry trades. What that means is trading pairs with big interest rate differentials. For example, using the strategy of long-only trades on AUD/JPY.

The idea is that positive rollover credits accumulate because of the large open trade volumes.

I’ve never used this approach before. Because the risks are that currency pairs with carry opportunities often follow strong trends. These are usually interspersed by steep corrective phases as carry positions are unwound (reverse carry positioning).

This can happen violently. For example if there are unexpected changes in the interest rate cycle, or if there’s a sudden change in risk appetite in which case funds tend to move away from high-yielding currencies very quickly (read more about carry trading.)

Getting caught the wrong side of one of these corrections is just too big a risk in my view. Over the long term, Martingale suffers in trending markets (see return chart – opens in new window).

It’s also worth keeping in mind many brokers subject carry interest to a significant spread – which makes all but the highest yielding carry trades unprofitable. Some retail brokers don’t even credit positive rollovers at all. That’s a consequence of being at the end of the “food chain”.

The low yields mean your trade sizes need to be big in proportion to your capital for carry interest to make any difference to the outcome. As I said above, this is too risky with Martingale.

A strategy better suited to trending is Martingale in reverse.

Using Martingale as a Yield Enhancement

As I mentioned before, I don’t suggested using Martingale as your main trading strategy. For it to work properly, you need to have a big drawdown limit relative to your trade sizes. If you’re trading with a sizable chunk of your capital, you’d risk “going broke” on one of the downswings.

The most effective use of Martingale in my experience is as a yield enhancer. I’ve applied the strategy I’m going to describe below over a 3 year time frame – with good results. This was done by trading the liquid part of a big portfolio. By capping the drawdown at 4% of the free cash and incrementally increasing it, I was able to get a reliable 0.4-0.6% overall return per month.

The least risky trading opportunities for this are pairs trading in tight ranges.

For example I’ve achieved good results using EUR/GBP and EUR/CHF during flat consolidation phases. In the case of EUR/CHF intervention policy is likely to see the pair trading in a tight range for now. Likewise EUR/GBP tends to have long range bound periods, which favors this type of “swing” strategy.

But you have to watch out for break-outs of significant new trends – watch out especially around key support/resistance levels.

Trading pairs that have strong trending behavior like Yen crosses or commodity currencies can be very risky.

You can download the complete trading system, as described below, in my Excel spreadsheet.

My program trading module, which was effectively a Martingale robot (EA) was created from this basic design.

Calculate Your Drawdown Limit

A good place to start is to decide the maximum open lots you’re able to risk. From this, you can work out the other parameters. To keep things simple, I’ll use powers of 2.

The maximum lots will set the number of double-down legs that can take place. So for example, if your maximum is 256 lots, this will allow doubling-down 8 times – or 8 legs. The relationship is:

Max lots = 2Legs

If you close the final trade on reaching its stop loss, your maximum drawdown would then be:

Drawdown $ < Max lots x ( 2 x Stop Loss ) x Lot size

So, with 256 lots (micro lots), and a stop loss of 40 pips, that would give a maximum drawdown of $2,048 (depending on your currency).

Tip Work out the average number of trades you can handle before a loss – use the formula 2Legs+1. So in the example here that’s just 29, or 512 trades. So after 512 trades, you’d expect to have a string of 9 losers given even odds. This would break your system.

You can use my lot calculator in the Excel workbook to try out different trade sizes and settings.

The best way to deal with drawdown is to use a ratchet system. So as you make profits, you should incrementally increase your lots and drawdown limit. For example, see the table below.

| Iteration # | Realized equity | Drawdown allowed | Profit |

| 1 | $1,000 | $1,000 | $25 |

| 2 | $1,025 | $1,025 | $5 |

| 3 | $1,030 | $1,030 | -$10 |

| 4 | $1,020 | $1,020 | $5 |

| 5 | $1,025 | $1,025 | $20 |

Copyright © 2015 Forexop.com

Table 5: Ratcheting up the drawdown limit as profits are realized.

This ratchet is automatically handled in the trading spreadsheet. You just need to set your drawdown limit as a percentage of realized equity.

Warning Since Martingale trading is inherently risky your capital at risk shouldn’t ever exceed 5% of your account equity. See forexop’s money management section for more details.

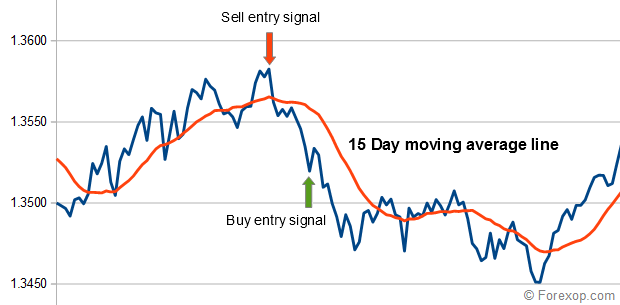

Decide On An Entry Signal

When the rate moves a certain distance above the moving average line, I place a sell order. When it moves below the moving average line, I place a buy order. This system is basically trading false break-outs, also known as “fading”.

In my system, I’m using the 15 point moving average (MA) as my entry signal. The length of moving average you choose will vary depending on your particular trading time frame.

This is a very simple, and easily implemented indicator. There are more sophisticated methods you could try out. For example using the Bollinger channel or other moving averages. Personally I find the simplest approaches are as good as any.

Whichever signal you decide to use, it should indicate that there’s a high probability of a retracement to the original trend rather than breaking-out in a new direction. So fading on break-out moves is what you should try to achieve.

Set The Take Profit and Stop Loss

The next two points to think about are

- When to double-down – this is your virtual stop loss

- When to close – your “take profit level”

When to double-down – this is a key parameter in the system. The “virtual” stop loss means you assume at that point the trade has gone against you. It’s a loser. So you double your lots.

Choose too small a value and you’ll be opening too many trades. Too big a value and it impedes the whole strategy.

The value you choose for your stops and take profits should ultimately depend on the time-frame you’re trading and the volatility. Lower volatility generally means you can use a smaller stop loss. I find a value of between 20 and 70 pips is good for most situations.

When to close Trades in Martingale should only be closed when the “entire system” is in profit. That is, when the net profit on the open trades is at least positive. As with grid trading, with Martingale you need to be consistent and treat the set of trades as a group, not independently.

A smaller take profit value, usually around 10-50 pips, often works best in this setup.

There are a couple of reasons for this.

- A smaller take profit level, has a higher probability of being reached sooner so you can close while the system is profitable.

- The profit gets compounded because the lots traded increase exponentially. So a smaller value can still be effective.

Using a smaller take profit doesn’t alter your risk reward. Although the gains are lower, the nearer win-threshold improves your overall trade win-ratio.

Simulations

The table below shows my results from 10 runs of the trading system. Each run can execute up to 200 simulated trades. I started with a balance of $1,000 and drawdown limit 100% of that amount. The drawdown limit is automatically ratcheted up or down each time the realized P&L changes.

| Run # | Profit | Run. Balance | Drawdown limit | Worst drawdown | Return |

| 1 | $22 | $1022 | $1,000 | -$5.25 | 2.2% |

| 2 | $36 | $1,058 | $1022 | -$38.43 | 3.4% |

| 3 | $37 | $1,095 | $1,058 | -$31.50 | 3.4% |

| 4 | $147 | $1,242 | $1,095 | -$346.86 | 11.8% |

| 5 | $141 | $1,383 | $1,242 | -$153.31 | 10.2% |

| 6 | $205 | $1,588 | $1,383 | -$377.81 | 12.9% |

| 7 | $46 | $1,634 | $1,588 | -$63.44 | 2.8% |

| 8 | $101 | $1,735 | $1,588 | -$87.12 | 5.8% |

| 9 | $35 | $1,770 | $1,588 | -$12.70 | 2.0% |

| 10 | $26 | $1,796 | $1,588 | -$10.20 | 1.4% |

Copyright © 2015 Forexop.com

Table 6: Simulation results from the spreadsheet.

My final balance was $1,796 which gives an overall return of 79.6% on the initial starting amount.

The chart below shows a typical pattern of incremental profits. The orange line shows the relatively steep drawdown phases.

The spreadsheet is available for you to try this out for yourself. It is provided for your reference only. Please be aware that use of the strategy on a live account is at your own risk.

#FX

#Forex

#Martingale

#MartingaleSystem

#Forex

#Martingale

#MartingaleSystem

Source : ForexOP

0 Response to "What is Martingale System?"

Thanks for give comment.